The scale of Ethereum de-pledge has reached a new high, what is the risk of selling pressure?

Original author: Nancy, PANews

At present, the divergence between long and short Ethereum is becoming more and more obvious. As ETH prices hit highs, the demand for staking withdrawals has increased significantly, raising concerns about potential downside risks. Will Ethereum's massive selling pressure occur as expected?

Driven by multiple factors, the scale of Ethereum staking unstaking hits a new high

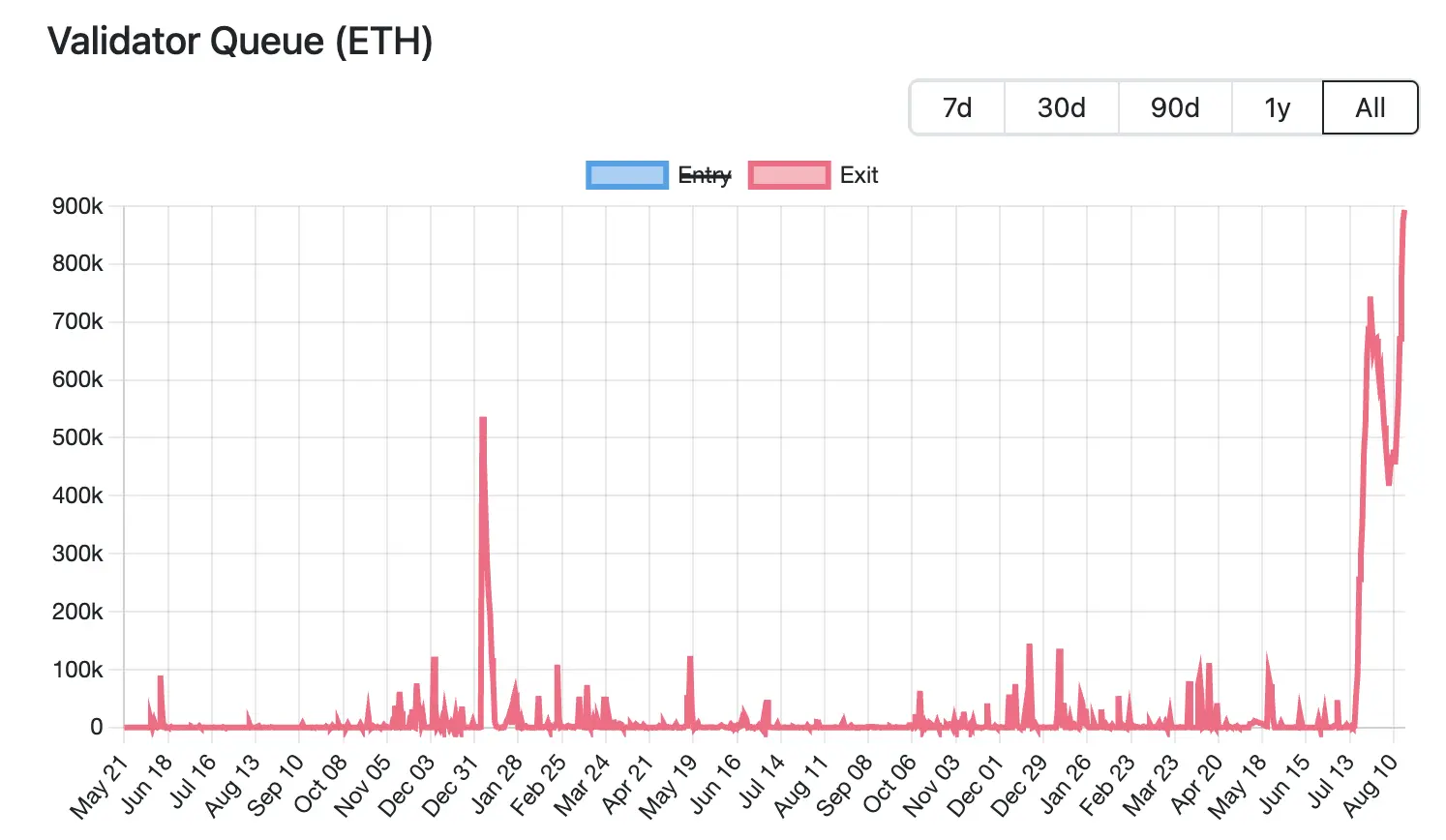

Currently, the scale of Ethereum's unstaking has reached an all-time high. According to Validator Queue data, as of August 18, more than 87,000 ETH (worth approximately $3.76 billion) are queuing up to exit the Ethereum network, a record high, and have increased for 6 consecutive days, with an expected wait of 15 days and 4 hours. In contrast, there are only about 26,000 new staked ETH (about $1.12 billion) waiting to enter, and the activation delay is expected to be about 4 days and 12 hours.

Currently, the scale of Ethereum's unstaking has reached an all-time high. According to Validator Queue data, as of August 18, more than 87,000 ETH (worth approximately $3.76 billion) are queuing up to exit the Ethereum network, a record high, and have increased for 6 consecutive days, with an expected wait of 15 days and 4 hours. In contrast, there are only about 26,000 new staked ETH (about $1.12 billion) waiting to enter, and the activation delay is expected to be about 4 days and 12 hours.

The large-scale exit of this round of pledge is driven by multiple factors, involving market strategy adjustments, institutional capital flows, and profit-taking needs brought about by price fluctuations.

ETH lending rates have risen sharply, leading to a shock to leverage strategies, which has spurred validators to exit the queue. Last month, a significant amount of ETH was withdrawn from the Aave lending pool, leading to a tight supply of ETH on the platform, which drove a significant surge in borrowing rates. According to official website data, Aave's annual interest rate on ETH lending climbed from about 2.5% to 10.6% in July, far exceeding Ethereum's staking yield of about 3% at that time.

This rise in interest rates breaks the trading logic of cyclical arbitrage. Originally, investors could use their pledged ETH as collateral and borrow more ETH for leverage. However, this leverage model lost its appeal after a sharp rise in interest rates, forcing traders to close their positions, unstake to repay loans or reduce leverage, exiting demand.

The rise in lending rates has also exacerbated the de-anchoring of LST/LRT (e.g., stETH, weETH) from ETH. For example, Dune data shows that the discount rate between stETH and ETH reached 0.4% in July. This has led arbitrageurs to choose to buy liquid staked tokens at low prices on the secondary market and earn the spread by exchanging the full ETH value after unstaking, thereby driving further congestion in the Ethereum staking queue.

At the same time, although the market has not yet seen systematic liquidations due to price unanchoring, underlying pressure has further pushed investors to leave early. According to a recent analysis by Jlabs Digital analyst Ben Lilly, stETH is currently being withdrawn from Lido, and 32% of stETH (wstETH) is used as collateral for lending protocols, and depegging may mean a large-scale liquidation of lending protocols. Meanwhile, 278,000 wstETH are in a "high risk" state (high risk is defined as a health factor between 1-1.1 times).

Juan Leon, senior investment strategist at Bitwise, also said that staking tokens like stETH can be traded at a discount, and the discount will reduce the value of collateral, which can trigger risk cutting, hedging and even liquidation, which will eventually lead to ETH spot sell-offs.

For this reason, many investors choose to exit, and some whales even choose to cut their flesh to cash out quickly. For example, Lookonchain recently monitored that a whale gave up queuing up to exit staking, directly exchanged 4,242.4 stETH for 4,231 ETH (worth $18.74 million), and deposited it into Kraken for sale, resulting in a direct loss of 11.4 ETH (approximately $50,500).

ETH's massive staking exit is also associated with the shift of funds to new staking protocols. As Ethereum's investment focus shifts from retail to institutional, its staking market landscape is undergoing significant changes. According to Dune data, as of August 18, three of the top five staking protocols are centralized institutions: Binance, Coinbase, and Figment. In the past month, Lido, ether.fi, and P2 P.og had the highest ETH outflows, with Lido exceeding 279,000 ETH in a single month, and its market share fell to 24.4%, hitting a record low. In contrast, Figment saw an inflow of over 262,000 ETH in a single month, making it the biggest winner.

Behind this migration trend is the multiple needs of institutions for compliance and stability, such as the need for clear legal entities and compliance processes, while decentralized protocols are difficult to meet regulatory requirements. Decentralized network nodes are scattered, difficult to fully audit, and nearly impossible to achieve global KYC. Centralized institutions can clearly bear the responsibility for node failures, while the responsibilities of decentralized protocols are scattered, which does not meet risk management expectations. There is uncertainty about the DAO voting mechanism, lack of decision-making stability for institutions, etc. In short, institutional funds value compliance, responsibility, and stability over decentralization. This also means that in the ETH staking market, decentralized protocols are gradually shifting to a defensive stance, while centralized staking institutions continue to expand their share with compliance and stability.

Behind the rise in the scale of ETH staking unstakes, the demand for profit-taking brought about by rising prices is also one of the driving factors. CoinGecko data shows that since April this year, the price of ETH has rebounded by about 223.7% from its lows. Such a rapid rise has provided considerable floating profits for early stakers, prompting some investors to choose to unstake and lock in profits, thereby increasing the liquid supply pressure of ETH in the short term.

Although the

scale of Ethereum staking unstaking has reached a record high, raising concerns about selling pressure, it may provide some support for ETH in view of the limited pace of release and the continued increase in institutional holdings.

On the one hand, as mentioned above, there are multiple factors behind this round of de-pledge, including the liquidation of circular strategies, arbitrage demand, and transfers to other stakers. This means that not all unstaked ETH goes straight to the market for sell-offs.

On the other hand, Ethereum's PoS mechanism has strict restrictions on validator withdrawals, requiring each validator to stake 32 ETH to participate in network consensus, while to ensure network stability, only 8–10 validators are allowed to withdraw per epoch (approximately 6.4 minutes). As the demand for validators to exit increases, the waiting queue lengthens significantly. It is currently expected that this portion of unstaked ETH will take about 15 days and 4 hours before it can actually be released to the market, so there will be no impact on liquid supply in the short term.

In addition, judging from market data, Ethereum currently has more than 61,000 ETH staking exit demand, but the increase in institutional investors' holdings can cover potential selling pressure. According to strategicethreserve.xyz data, as of August 18, the cumulative number of ETH held by Ethereum Reserve companies and various ETH spot ETFs reached 10.26 million ETH, accounting for 8.4% of the total supply of Ethereum. In the past half month, institutions have increased their holdings of ETH by more than 1.83 million, far exceeding the scale of this round of unstaking. If the trend of increasing holdings continues, it can effectively absorb potential selling pressure.

Overall, the recent high volatility in ETH prices may be a natural reaction to profit-taking and market sentiment fluctuations. Despite certain uncertainties and short-term volatility pressures in the market, Ethereum's overall confidence has not wavered, especially the persistence of institutional funds, which has further enhanced market resilience.

Click to learn about ChainCatcher's recruitment positions

Recommended reading:

Vitalik's latest interview: Ethereum's road to the world ledger and the development of the AI era

dialogue Oppenheimer Executive Director: Coinbase Q2 Transaction revenue falls short of expectations, which businesses will become new growth points?

Conversation with TD Cowen, Head of Research: A deep dive into Strategy's Q2 earnings report, what's the key behind the $10 billion net income?